Enhanced Due Diligence (EDD) for Banks 2026: Regulatory Requirements and AI Automation

Quick Answer Banks are required to apply Enhanced Due Diligence (EDD) under FATF Recommendations 10 and 12, EU AMLD6, UK Money Laundering Regulations 2017, and the US Bank Secrecy Act. Mandatory triggers include correspondent banking relationships, politically exposed persons (PEPs), high-risk jurisdiction exposure, and complex beneficial ownership structures. EDD requires source-of-funds verification, UBO mapping, senior management approval, and enhanced ongoing monitoring — with all findings d

Scoreplex

May 21, 2026 · 10 min read

Disclaimer

This information is for general purposes only and does not constitute legal or compliance advice. Consult a qualified professional for specific guidance.

Quick Answer Banks are required to apply Enhanced Due Diligence (EDD) under FATF Recommendations 10 and 12, EU AMLD6, UK Money Laundering Regulations 2017, and the US Bank Secrecy Act. Mandatory triggers include correspondent banking relationships, politically exposed persons (PEPs), high-risk jurisdiction exposure, and complex beneficial ownership structures. EDD requires source-of-funds verification, UBO mapping, senior management approval, and enhanced ongoing monitoring — with all findings documented in an audit-ready case file. For the full EDD framework, see the Enhanced Due Diligence (EDD): Complete Guide for Compliance Teams.

Banks operate under the most demanding Enhanced Due Diligence (EDD) obligations in the financial sector. A single correspondent banking relationship exposes an institution to AML risk across multiple jurisdictions simultaneously. A high-net-worth client with opaque beneficial ownership triggers documentation requirements that standard Customer Due Diligence cannot satisfy. And the regulatory consequences of insufficient EDD are measurable: HSBC's $1.9 billion AML settlement and Deutsche Bank's $630 million penalty represent the compliance floor, not the ceiling.

This guide covers the regulatory framework governing Enhanced Due Diligence (EDD) for banks in 2026, the specific triggers that mandate escalation, the three operational challenges compliance teams consistently face, and what AI automation changes about the economics of a high-volume EDD programme.

Regulatory Requirements for Enhanced Due Diligence (EDD) in Banks (2026)

Enhanced Due Diligence (EDD) obligations for banks derive from four regulatory frameworks that operate in parallel. Compliance teams working across jurisdictions must satisfy all applicable requirements simultaneously — not the most permissive one.

FATF Recommendations 10 and 12 establish the global risk-based baseline. FATF Recommendation 10 requires financial institutions to apply EDD measures for higher-risk business relationships, including enhanced ongoing monitoring and source-of-funds verification. Recommendation 12 mandates EDD specifically for politically exposed persons, requiring senior management approval and enhanced scrutiny of the source of wealth. All major jurisdictions trace their EDD rules back to this framework.

EU Anti-Money Laundering Directive 6 (AMLD6) codifies FATF requirements into binding EU law. Article 18 requires EDD for business relationships with persons from high-risk third countries identified by the European Commission. Article 19 applies mandatory EDD to all correspondent banking relationships with institutions outside the EU — requiring banks to assess the respondent institution's AML/CFT controls, document the division of responsibilities, and obtain senior management approval before establishing the relationship.

UK Money Laundering Regulations 2017 (MLRs) implement FATF standards post-Brexit under domestic law. Regulation 33 sets out enhanced due diligence measures, including enhanced ongoing monitoring for high-risk relationships and the requirement to examine the background and purpose of complex or unusual transactions.

US Bank Secrecy Act (BSA) and FinCEN CDD Final Rule govern EDD for US-chartered and US-operating banks. The FinCEN CDD Final Rule requires banks to identify and verify beneficial owners at a 25% ownership threshold plus one controlling person per legal entity customer. For elevated-risk relationships, institutions must apply enhanced scrutiny proportionate to the assessed risk level.

The EBA Guidelines on ML/TF Risk Factors supplement the AMLD framework with sector-specific guidance on how banks should calibrate their EDD programmes to customer type, product, delivery channel, and geographic risk.

The table below summarises the key EDD obligations by jurisdiction:

For a full cross-jurisdictional comparison of EDD requirements, see EDD vs CDD: Key Differences Explained.

When Are Banks Required to Apply Enhanced Due Diligence (EDD)?

Standard Customer Due Diligence is the baseline. Enhanced Due Diligence (EDD) is mandatory when the risk profile of a customer, relationship, or transaction exceeds what standard CDD can adequately address. For banks, six triggers consistently appear across all major regulatory frameworks.

1. Correspondent banking relationships. Any bank establishing or maintaining a correspondent account with a respondent institution outside its home jurisdiction must apply Enhanced Due Diligence (EDD) under AMLD6 Article 19 and equivalent BSA guidance. This requires assessing the respondent's AML/CFT controls, documenting the division of EDD responsibilities, and obtaining senior management approval before the relationship begins.

2. Politically exposed persons (PEPs). Clients who hold or have held prominent public functions — and their immediate family members and known close associates — trigger mandatory EDD under FATF Recommendation 12 across all jurisdictions. Senior management approval and source-of-wealth verification are required from the outset of the relationship.

3. High-risk jurisdiction exposure. Customers, counterparties, or transaction flows connected to jurisdictions on the FATF grey list, EU high-risk third-country list, or OFAC-sanctioned territories require Enhanced Due Diligence (EDD) regardless of the customer's own risk profile.

4. Complex or opaque ownership structures. Legal entity customers with multi-layered ownership chains, nominee shareholders, or beneficial owners in high-risk jurisdictions require enhanced UBO mapping that goes beyond the standard 25% threshold identification.

5. Private banking and high-net-worth individuals. Wealth management and private banking relationships involving large asset transfers, offshore structures, or clients from high-risk industries require source-of-wealth analysis and enhanced ongoing monitoring by default at most institutions.

6. Unusual or unexplained transaction patterns. Transactions that are inconsistent with the stated business purpose, involve structuring activity, or show sudden changes in volume or geography require Enhanced Due Diligence (EDD) review and documented rationale — even for existing low-risk customers.

For a comprehensive list of all eight EDD triggers across sectors, see When Is Enhanced Due Diligence Required?

Top 3 Enhanced Due Diligence (EDD) Challenges for Banks

Banks don't struggle with understanding EDD requirements. They struggle with executing them at scale, across jurisdictions, under exam pressure, without breaking onboarding timelines. Three operational challenges account for the majority of EDD programme failures.

Pain 1: Volume and analyst capacity.

Large banks process hundreds of EDD cases per month. Mid-size institutions face the same regulatory obligations with a fraction of the compliance headcount. A single manual Enhanced Due Diligence (EDD) review — covering registry verification, UBO mapping, sanctions screening, adverse media, and document validation — takes 30 to 240 minutes of analyst time per case. At 500 cases per month, that is between 250 and 2,000 analyst hours consumed by data gathering alone, before any judgment or documentation work begins. The result is a queue that grows faster than it is resolved, delayed onboarding, and revenue held in review.

Pain 2: Correspondent banking across multiple jurisdictions.

Correspondent banking EDD is structurally more complex than standard customer EDD. A single respondent institution may operate across five jurisdictions, hold licences under different regulatory regimes, and present ownership structures that require cross-border registry checks in languages the reviewing team does not read. Manual workflows built on individual analyst research — searching registries one by one, translating documents, and assembling findings into a case narrative — cannot scale to the coverage that AMLD6 and BSA guidance requires. Coverage gaps in correspondent banking EDD are consistently flagged in regulatory examinations as a systemic control weakness. For documentation standards that regulators examine during audits, see EDD Documentation Requirements 2026.

Pain 3: Audit-ready documentation under regulatory scrutiny.

Banks are among the most heavily examined institutions in any jurisdiction. Regulatory expectations for Enhanced Due Diligence (EDD) documentation have risen significantly following major enforcement actions: examiners now expect a complete, traceable, evidence-linked case file — not a summary memo and a screenshot. Adverse media reviews must reference named sources with dates. Sanctions screening must log the lists checked, match rationale, and disposition. UBO structures must be supported by source documents, not analyst assertions. Building that level of documentation manually, consistently, across every case, at volume, is where most bank EDD programmes fail the exam — not because the risk judgments were wrong, but because the paper trail was incomplete.

How Scoreplex Automates Enhanced Due Diligence (EDD) for Banks

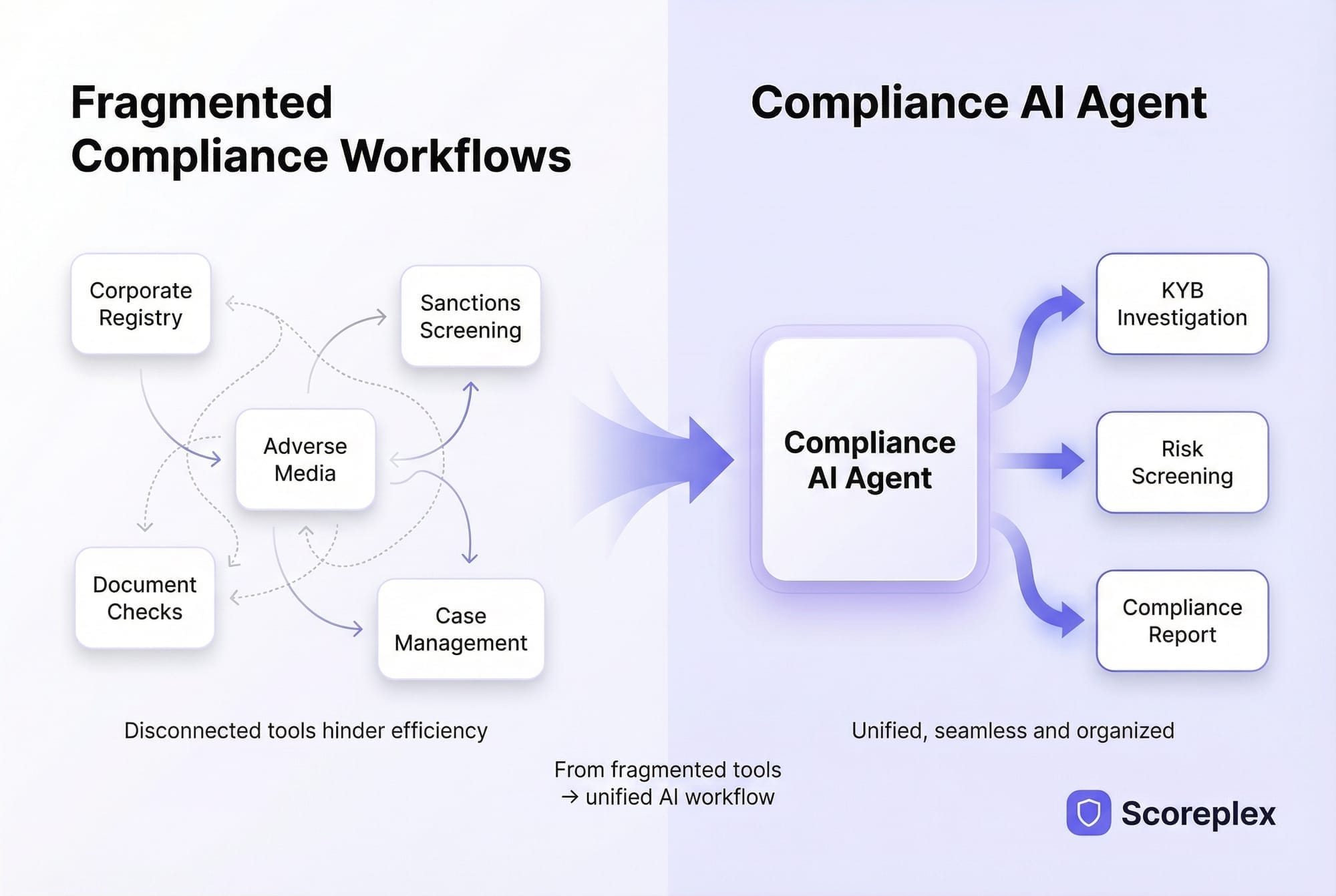

Scoreplex is an AI-native Enhanced Due Diligence (EDD) platform built for compliance teams that need to run high-volume, cross-border business reviews without proportionally scaling analyst headcount. The platform consolidates six investigation layers — registry, ownership, sanctions, adverse media, web presence, and documents — into one evidence-linked workflow and generates an audit-ready case file as output.

The table below maps each EDD requirement banks face to the specific Scoreplex capability that addresses it:

What this replaces in practice. A manual Enhanced Due Diligence (EDD) review at a bank requires an analyst to query multiple registries individually, translate documents where necessary, run sanctions checks across separate tools, search adverse media in multiple languages, and then assemble findings into a case narrative. That process takes 30 to 240 minutes per case and costs $10 to $80 in direct analyst time. Scoreplex completes the same scope in 5 to 30 minutes at $2 to $5 per case — across all six investigation layers simultaneously.

For correspondent banking specifically, Scoreplex covers 140+ business jurisdictions and screens against 325+ global watchlists in a single workflow — removing the manual, registry-by-registry research that makes correspondent banking EDD operationally expensive. Results are returned in the analyst's working language via 200+ language translation, eliminating document translation as a bottleneck.

Adverse media screening applies configurable risk-keyword categories — fraud, money laundering, sanctions, bribery, corruption, investigation — and reduces false positives by up to 85% compared to keyword-only manual searches. Every finding is source-attributed with a link, date, and relevance assessment, satisfying the documentation standard regulators expect to see during examination.

The output is a single, structured, evidence-linked case file. No separate tool exports, no manual assembly, no undated screenshots. For a detailed breakdown of what audit-ready EDD documentation requires, see EDD Documentation Requirements 2026. For a direct cost comparison of manual versus AI-automated workflows, see Manual vs AI Enhanced Due Diligence.

Return on Investment: Enhanced Due Diligence (EDD) Automation for Banks

The economics of automating Enhanced Due Diligence (EDD) are straightforward to model. The inputs are case volume, current cost per case, and current time per case. The outputs are cost reduction, time recovery, and analyst capacity freed for judgment work rather than data gathering.

At 500 EDD cases per month, the operational difference compounds quickly. At a conservative $10 per manual case, monthly cost is $5,000. At $2 per automated case, monthly cost is $1,000. That gap — $4,000 per month — represents $48,000 in annual direct savings at the low end of manual cost estimates. At the $80 upper bound for complex correspondent banking cases, the same 500-case volume costs $40,000 per month manually versus $2,500 with AI automation — a difference of $37,500 per month, or approximately $219,000 per year in recovered analyst spend.

That figure does not account for the indirect costs that manual EDD programmes carry: delayed client onboarding, failed regulatory examinations due to incomplete documentation, and the senior management time consumed by exception-handling and RFI loops. For the full cost breakdown methodology, see EDD Cost Breakdown: Manual Reviews vs AI Automation.

About Scoreplex

Scoreplex is an AI platform that automates customer due diligence, minimizes false positives, streamlines document verification, and generates comprehensive narrative reports.

How it works: From a single company input, it produces a complete business risk profile, including::

- Official registry checks with UBO identification and full ownership chains

- Global sanctions and PEP screening

- Real-time adverse media monitoring with structured events and source attribution

- Automated document verification (incorporation records, address validation)

- Website analysis and cross-checks of company details, products, contacts, and locations

- Product and customer review analysis (Trustpilot, G2, Google Reviews)

- Social media analysis of corporate accounts and profiles of founders and directors

- High-risk country exposure assessment based on aggregated signals

- A structured risk summary highlighting red flags, rationale, and direct source links

Built for Faster, Smarter Decisions:

- 10× faster reviews through end-to-end automation

- Up to 10× lower costs compared to traditional service providers

- Significantly fewer false positives driven by registry-first matching and transparent risk signals

Frequently Asked Questions: Enhanced Due Diligence (EDD) for Banks

What Enhanced Due Diligence (EDD) requirements apply to banks?

Banks must apply Enhanced Due Diligence (EDD) under FATF Recommendations 10 and 12, EU AMLD6, UK Money Laundering Regulations 2017, and the US Bank Secrecy Act. Requirements include source-of-funds verification, UBO mapping, senior management approval, enhanced ongoing monitoring, and audit-ready documentation for all elevated-risk relationships.

When is Enhanced Due Diligence (EDD) mandatory for correspondent banking?

Enhanced Due Diligence (EDD) is mandatory for all correspondent banking relationships with institutions outside the EU under AMLD6 Article 19, and for equivalent cross-border relationships under BSA guidance. Banks must assess the respondent institution's AML/CFT controls, document the division of EDD responsibilities, and obtain senior management sign-off before establishing the relationship.

What documents must banks retain for Enhanced Due Diligence (EDD) compliance?

Banks must retain enhanced identity verification records, source-of-funds and source-of-wealth evidence, UBO structure charts with supporting documents, PEP and sanctions screening logs with match disposition, adverse media review records with named sources and dates, senior management approval records, and ongoing monitoring schedules. All records must be retrievable on demand during regulatory examination.

How long does a bank Enhanced Due Diligence (EDD) review take?

A manual Enhanced Due Diligence (EDD) review covering registry verification, UBO mapping, sanctions screening, adverse media, and document validation takes 30 to 240 minutes per case. AI-automated EDD platforms complete the same scope in 5 to 30 minutes, with full multi-jurisdictional coverage and an audit-ready output.

What is the cost of Enhanced Due Diligence (EDD) for banks?

Manual Enhanced Due Diligence (EDD) costs $10 to $80 per case in direct analyst time. At 500 cases per month, that represents up to $40,000 in monthly spend. AI automation reduces per-case cost to $2 to $5, delivering approximately $219,000 in annual savings at the same volume.

How do banks reduce false positives in Enhanced Due Diligence (EDD) adverse media screening?

False positives in adverse media screening are reduced through AI models that cluster related news events, apply configurable risk-keyword categories, and assess source credibility — rather than returning every keyword match as a separate alert. Scoreplex reduces adverse media false positives by up to 85% compared to keyword-only manual searches, with every finding source-attributed and dated.

Does Enhanced Due Diligence (EDD) apply to all bank customers?

No. Enhanced Due Diligence (EDD) applies when a customer, relationship, or transaction presents elevated risk that standard Customer Due Diligence cannot adequately mitigate. Mandatory triggers for banks include PEPs, correspondent banking relationships, high-risk jurisdiction exposure, complex ownership structures, private banking clients, and unusual transaction patterns inconsistent with the stated business purpose.